Key Takeaways from 4Q 2023

- 2023 was a strong year for financial markets, thanks to a year-end rally in November and December.

- Although the Magnificent Seven stocks were the year’s top performers, it is important to look beyond the current moment’s hot area and try to maintain a diversified portfolio through a full market cycle.

- Cash maintains an attractive yield at over 5%, but investing for long-term success means investors should own bonds in a variety of sectors and duration, not just focus on what is attractive right now.

After an ugly third quarter and even start to the fourth quarter, markets regained their footing in November and finished the year strongly in positive territory. Consistent with how markets have traded the past 18 months, the pivot coincided with the Federal Reserve’s meeting on November 1. Following that meeting, Chairperson Jerome Powell announced that the Committee anticipates rate cuts in 2024. While he did give the number of cuts they expect over the coming year, the Fed’s estimates rarely play out as anticipated; therefore, investors may be able to expect the Fed Funds Rate to be lower at the end of 2024 than where it began.

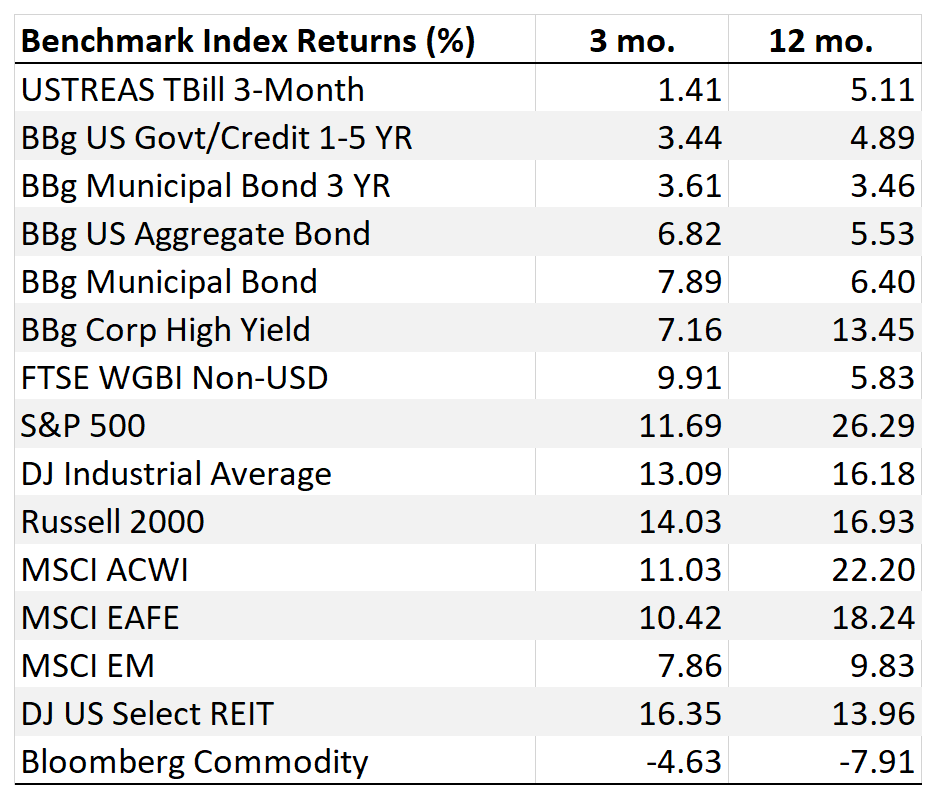

Markets’ reactions to the Fed’s announcement were responsible for much of the strong performance experienced last year, except for U.S. large cap stocks, which experienced strong returns all year. Bonds ended the third quarter with negative year-to-date returns and closed the year up 5.5%. Most U.S. stocks, other than large growth, driven by the Magnificent Seven, were slightly positive to start the fourth quarter and ended the year with a return in the mid-teens.

For an investment portfolio to have performed well during 2023, it had to be invested for November and December. Thinking back to October, investors were not optimistic. We were in the midst of a three-month decline in equity markets, the 10-year U.S. Treasury yield was just under 5%, and recessionary fears loomed, all the while cash was out there yielding more than 5%. Once the calendar turned to November, we were reminded how quickly markets can change. In the remaining two months of the year, the 10-year U.S. Treasury yield fell to under 4% (bond prices rise as yields decline), large cap stocks rose 14%, and small cap stocks were up over 20%. Returns that come this quickly can only be captured by already being invested with exposure to all areas of markets, not just those doing best.

Stocks

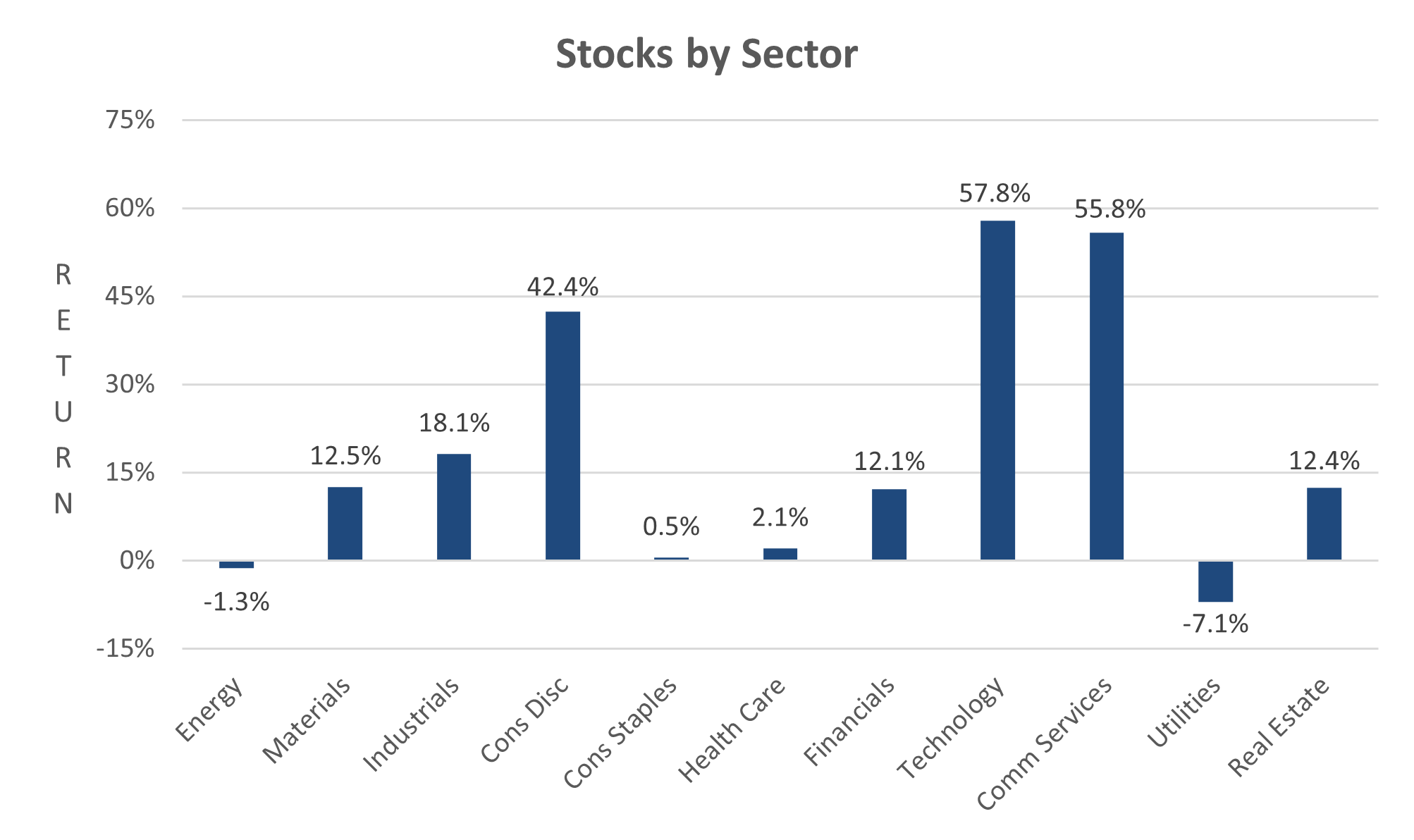

The S&P 500 Index posted a 26% gain in 2023, closing the year just under its all-time high. One aspect that stands out is the dispersion between the index’s sectors. Two sectors ended the year up by over 50% (information technology and communication services), while two sectors posted negative returns (energy and utilities). This scenario is the opposite of what occurred in 2022 when energy was up 65%, and information technology was the lowest performing sector, falling -28%—again, exemplifying the importance of staying invested in a diversified portfolio across all sectors and regions. It is difficult to sell a top performer to buy an underperformer, but trying to maintain a diversified portfolio can help take those decisions out of the equation.

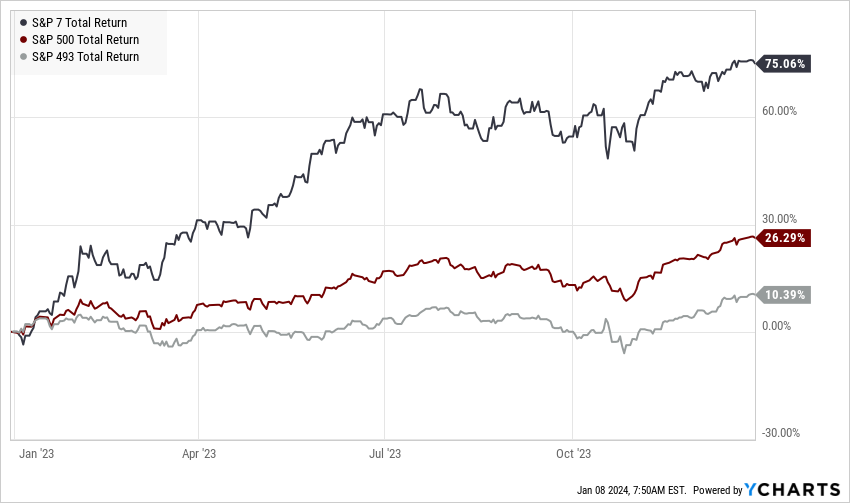

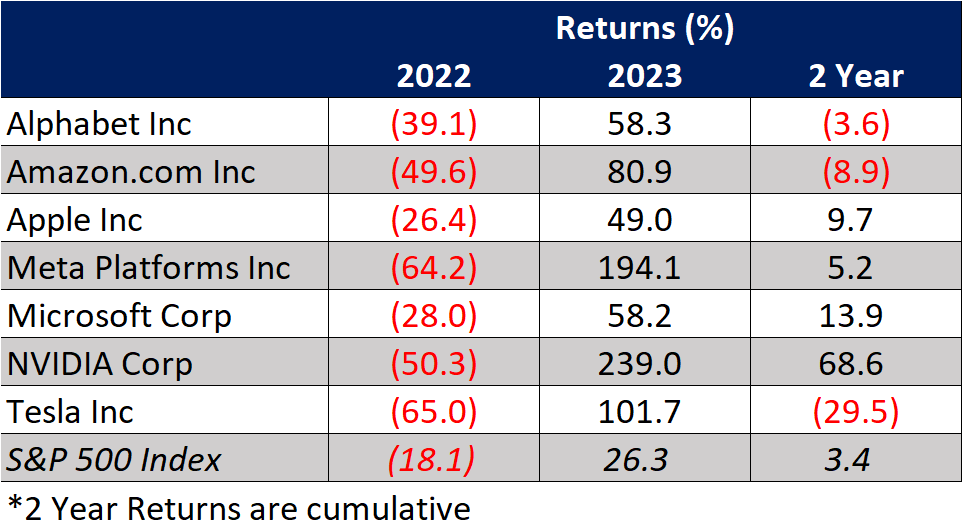

We can attribute much of the information technology and communication services sectors’ outperformance to the Magnificent Seven stocks, the coined term given to the stocks Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla. While a portfolio of just these stocks generated a highly attractive 75% return last year, it was quite the opposite scenario in 2022. During 2022, each of the Magnificent Seven stocks performed significantly worse than the S&P 500 Index’s -18% return. Even over the past two years, Nvidia is the only Magnificent Seven stock to have beat the index significantly. Tesla was up 100% in 2023, yet their return over the prior two years was still -30% on a cumulative basis.

Last year was the year for the Magnificent Seven stocks, but an investment time horizon is much longer than any one-year period. Every short time frame we explore, there will be clear winners and losers. However, the losers of one period can be winners of the next, exemplifying why it is important to try to maintain a diversified portfolio. Winners will not stay winners forever, which is why it is helpful to maintain a disciplined portfolio rebalancing schedule, to sell winners high and reinvest those proceeds in underperforming areas of the market, which could be the winners of the future.

Bonds

Before exploring the bond market’s performance, a notable event of 2023 was that it was the first year since 1962 (when market data was first collected) that the yield curve was inverted for the entire year (meaning short-term yields were higher than longer-term yields). Looking at the chart below, why would investors want to make a loan for ten years when they could make a 2-year loan and earn more interest? Or, even better, they could invest in cash and earn close to the 5.3% rate set by the Fed.

Similar to how investors should not invest in only the Magnificent Seven in equity portfolios, they should not invest only in bonds with the highest yields right now. Just 18 months ago, cash yielded less than 1.5%; now, it’s over 5%. As the Fed begins cutting rates, cash yields can quickly change. Still, longer-duration bonds will be able to maintain a higher yield for longer because those rates are maintained until each bond matures. While investors do not want to give up all of what cash is currently yielding, they should try to diversify across the bond spectrum, owning cash and longer-term bonds that will maintain higher yields beyond when the Fed cuts rates on cash.

Aside from higher yields for longer, the other potential benefit of owning longer-term bonds is the protection they can provide in a recessionary environment. Forecasters have been predicting a recession for a while, and it has yet to hit. However, if/when we do enter a recessionary environment, duration is a portfolio’s friend. Although cash looks incredibly attractive right now, remember we are trying to invest for success over decades, not trying to pick the hottest areas in one specific moment.

Looking Ahead

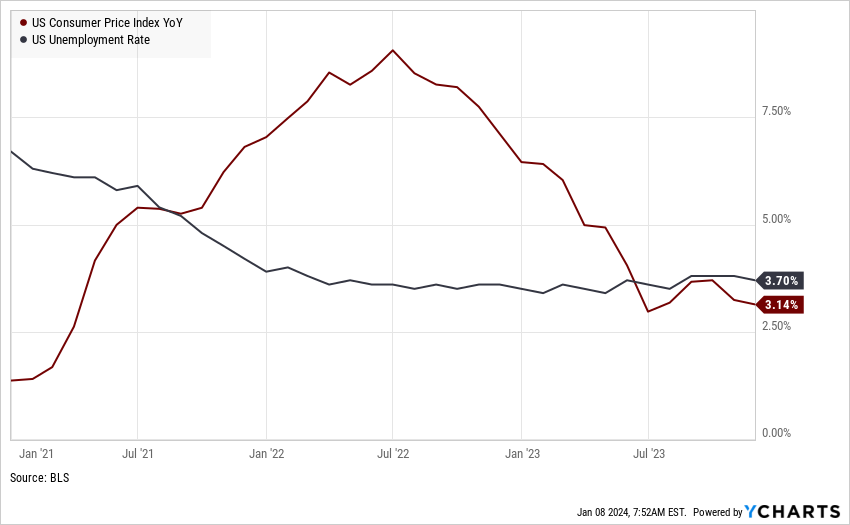

The discussion entering 2023 focused on whether the Fed could successfully deliver a soft landing (lowering inflation without causing a recession). While we still do not have a clear signal if the soft landing was delivered or not, inflation decreasing throughout the year, accompanied by a falling unemployment rate, is a strong start. Controlling inflation is an essential element to avoid a recession. Still, unemployment is an important factor since it’s hard to have a recession when people are working.

The average forecast for 2023 was a recession toward the end of the year and negative returns for the S&P 500 Index. We now know those outlooks were off, but that will not stop predictions for what could be in store for 2024. News stations will have a guest who correctly predicted an economic collapse over 15 years ago voicing their view of all the negative factors currently weighing on markets. That will be contradicted by someone expressing their opinions on all the positive reasons why markets will have a great year. The truth is no one can predict what markets will do over the next 12 months. No matter what firm is making headlines or the background of any individual, no one has a crystal ball to tell us what markets will do over the next year.

Investors should not spend time guessing what the next year might have in store because we do not know. The last year alone saw a regional banking crisis, continuation of the Ukraine/Russia war, the start of the Israel/Hamas war, multiple labor strikes, and several natural disasters, just to name a few, yet markets and economies continued to grow. Investors should follow a process of trying to maintain diversified portfolios and rebalancing back to target allocations to help remove emotional decisions in the short-term in favor of long-term success.