Key Takeaways from 1Q 2025

- On April 2nd, President Trump announced reciprocal tariffs, which exceeded market expectations and triggered a sharp sell-off in equity markets. Although portfolios have taken a hit, this marks the eighth time in the past twenty-five years that the stock market has declined by 15% or more. While the reasons for each decline may vary, we’ve experienced similar situations before and expect our portfolios to eventually recover, as they did after the previous seven occurrences.

- Before making any changes to your portfolios, it’s important to focus on your long-term plan. Money is held in bonds to provide protection during turbulent times like these; bonds will cover near-term spending needs while stocks work to recover from their losses.

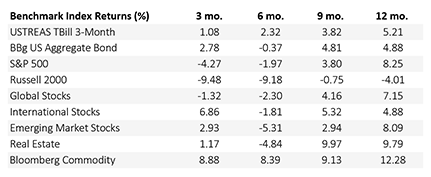

As we approached the end of the first quarter, I began to gather my thoughts for the upcoming review. The main theme would be “The Return of Diversification.” Over the past two-plus years, the Magnificent Seven stocks had been the dominant performers, but they became laggards this quarter. In contrast, international stocks gained value, and bonds provided stability within portfolios. While the headlines focused on poorly performing stocks, diversified portfolios generally held up well. Although some portfolios posted slight losses, many recorded gains during this three-month period, thanks to contributions from bonds and international stocks.

First Quarter Sector Returns as of 3/31/2025

On April 2nd, known as “Liberation Day,” markets took a significant hit, declining by 11% in just two days. The prevailing question of the year quickly shifted to “What now?” During a 48-minute speech delivered from the Rose Garden of the White House, global trade underwent a dramatic change, leading to a sharp drop in equity markets. Let’s break this down into two parts: First, we need to analyze what is happening in the markets and the economy. Second, we should consider how to adjust our portfolios in response.

What’s Happening?

Markets had anticipated tariffs, given President Trump’s longstanding support for them, which he has expressed for decades. He implemented tariffs during his first term and campaigned on this issue in the last three presidential elections. However, the “Liberation Day” tariffs came as a surprise because they were significantly higher than expected. At the beginning of the year, the U.S. imposed an average tariff of 2.5% on all imported goods. If all the tariffs announced on April 2nd, along with those introduced since the inauguration, are implemented, the average tariff on imports will rise to between 22% and 25%, maybe higher depending on which retaliation tariffs take hold. This would mark the highest average tariff rate since 1910.

At the beginning of the year, the average tariff rate that the U.S. faced on goods exported to other countries was 4.6%. As discussions about reciprocal tariffs unfolded, market analysts expected the proposed rates to be higher than this average, but they were surprised by the actual announcement, which was significantly different. What confused the markets the most was the Trump Administration’s approach of considering the U.S. trade deficit with each country, rather than focusing solely on the tariffs those countries imposed.

Average Tariff Rate on U.S. Goods Imports for Consumption

As consumers, one of the first thoughts of this new environment is the impact on prices. Tariffs are a tax on goods imported from other countries. Depending on each product, it will either fall to companies along the supply chain, it will be paid for by consumers, or, the most likely outcome, it will be a combination. The longer tariffs continue at these rates, companies and consumers will be making the decision to continue paying higher prices, finding a cheaper alternative, or hold off spending until this dispute is settled. All these decisions will have various impacts on inflation, deflation, and economic growth, but it is too early to get into any of those discussions.

Instead of trying to predict possible economic and stock market scenarios, let’s switch to our current portfolios. Remember, the best time to buy and the worst time to sell is when the environment feels and sounds terrible.

What Now?

When markets drop by 11% in just two days and the headlines push extreme narratives, it’s natural for investors to feel anxious and question their portfolio strategies. The straightforward answer is to stay the course. If you feel the urge to take action, remember that you’ve already prepared for this volatility. We have built a diversified portfolio specifically designed to achieve your goals. Although equities may not be performing well at the moment, bonds are fulfilling their role as stabilizers. For clients who need cash in the near future, we will sell bonds while we wait for equities to recover. While U.S. stocks have seen a sharp decline recently, international stocks have performed better this year. Diversification gives us choices; not all stocks behave the same way, so it’s important to have exposure to various sectors to minimize risk and create opportunities.

Unfortunately, none of us have a crystal ball to predict when the volatility will end. However, we have faced challenging times before. While we may not have experienced a situation with such a rapid increase in tariffs, we have endured a global pandemic that caused markets to drop by 35% in just a few weeks. We also faced a financial crisis that led to a significant decline in the housing market and equity markets, which dropped by over 50%. In all these situations, as well as many others, our portfolios have recovered because we remained committed to our strategy.

Although it may seem like there is no end in sight, markets will recover. Since 2000, the stock market has experienced a decline of 15% or more seven times, which averages to about once every three and a half years. Portfolios have faced similar situations before, and each time, we wonder how severe it will be and whether the market will ever bounce back. Every downturn presents a new opportunity. While we cannot predict how long it will take to overcome this latest period of volatility, we are confident that markets will navigate this challenge in the short term and continue to grow in the long term.

After Declines, Recoveries Have Followed