- Get organized

- Determine which assets may skip the probate process

- Probate for Small Estates

- Formal probate process

- PA Inheritance Tax Tables:

- Federal Estate Tax Table

Many families are surprised by the complexities of the probate process in Pennsylvania, which can lead to unexpected delays and financial burdens. Understanding how to settle an estate in PA can help ease the transition and help ensure a smooth distribution of assets.

The process of settling an estate in Pennsylvania involves naming a personal representative, collecting estate assets, filing appropriate forms with the Register of Wills, notifying heirs, providing public notice, paying all debts and taxes, and distributing the remaining assets to heirs named in the will or under the laws of intestacy if there is no will.

This article will briefly overview the necessary steps when settling an estate in Pennsylvania.

Documents You’ll Need to Settle an Estate in Pennsylvania

To settle an estate, you’ll need to gather documents that direct or impact the assets and beneficiaries of the estate. You’ll want to locate important documents like:

- Original will

- Death certificates – multiple copies may be required

- Irrevocable and/or revocable trust documents

- Real estate deeds

- Bank account, brokerage, and retirement account statements

- Life insurance policies

- Outstanding loan, credit card, and bill statements

- Previous year’s income tax returns

- Gift tax returns

Determine Which Assets May Skip the Probate Process

Assets owned jointly with another person usually skip probate and can be passed to the co-owner. Examples of likely jointly owned assets may include bank accounts, brokerage accounts, and real estate. Trust assets also pass outside of probate.

Additionally, assets that have beneficiary designations may skip the probate process. Assets that typically have beneficiary designations are retirement accounts, annuities, and life insurance policies.

Be sure to look for Transfer on Death (TOD) and Payable on Death (POD) account designations as well. TOD and POD accounts also may bypass probate and go directly to the named beneficiaries.

Small sums of cash up to $10,000 can be distributed from bank accounts to the surviving spouse or family members by providing a copy of the death certificate and receipt of paid funeral expenses (20 Pa. C.S.A. § 3101(b).

Up to $10,000 in wages may also be distributed to the employee’s surviving spouse or family members (20 Pa. C.S.A. § 3101(a)).

Life insurance proceeds of $11,000 or less may also be paid out to the decedent’s surviving spouse or family members if the executor of the estate does not stake a claim within 60 days of the decedent’s death (20 Pa. C.S.A. § 3101(d)).

Here’s a handy table that broadly breaks down which assets go through probate and which skip it.

| Asset Type | Goes Through Probate? | Notes |

|---|---|---|

| Joint bank account | ||

| Retirement account with beneficiary | ||

| Real estate solely in decedent’s name | ||

| TOD brokerage account |

Probate Process for Small Estates in Pennsylvania

If an estate has less than $50,000 in assets (excluding real estate, assets used to pay the decedent’s funeral expenses, and the assets that skip probate), the executor may file a request with the local probate court.

If the court allows, the executor may distribute estate assets without following the formal probate process.

Formal probate process in Pennsylvania

If the estate does not qualify for the above simplified probate, the formal probate process is used.

PA Probate Process With a Will

If there is a will, the listed executor must file the will with the Register of Wills in the decedent’s local probate court. At the same time, the executor will file a Petition for Probate form.

Download Allegheny County’s Petition for Probate

A filing fee is also required and is determined by the size of the estate and by county. The Register of Wills will issue a Letters of Testamentary to give the listed executor the authority to carry out the estate settlement process. These steps officially open the probate process.

The will may be “self-proving.” Self-proving wills included notarized statements signed by witnesses that watched the decedent sign the will. If the will is not self-proving, the executor must provide sworn statements from the witnesses.

What Happens if Someone Dies Without a Will in Pennsylvania?

When there is no will, an interested party – typically a family member – must file a Petition for Probate form with the Register of Wills in the county where the decedent resides. A filing fee is required, and the amount varies by both the size of the estate and by county.

Once approved, the Register of Wills will issue Letters of Administration, officially appointing a personal representative—also called an executor or administrator. Pennsylvania follows a legal priority for naming administrators: starting with the surviving spouse, then adult children, followed by other family members, creditors, or—if needed—another individual the court deems “fit” to serve as administrator.

After appointment, the administrator is responsible for notifying all heirs, beneficiaries, and the public that probate has begun. This includes sending written notice to heirs and publishing a legal announcement in a local newspaper.

Next, the personal representative must:

- Inventory all estate assets

- Submit the inventory to the probate court

- Pay off debts and taxes owed by the estate

- Sell estate property as needed to cover expenses

It’s also important to understand Pennsylvania’s inheritance tax, which applies to many inherited assets–even if they’re not part of the probate estate. Taxable assets may include retirement accounts, annuities, and transfer-on-death (TOD) or payable-on-death (POD) accounts. However, life insurance policies are exempt from Pennsylvania’s Inheritance tax.

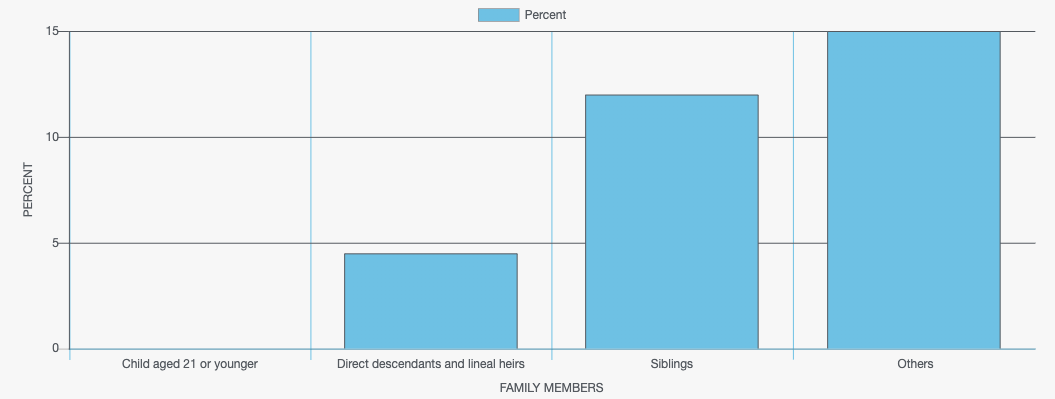

PA Inheritance Tax Tables:

- 0 percent on transfers to a surviving spouse or to a parent from a child aged 21 or younger. Also, transfers to charitable organizations, exempt institutions and government entities are exempt from inheritance tax.

- 4.5 percent on transfers to direct descendants and lineal heirs

- 12 percent on transfers to siblings

- 15 percent on transfers to others

Filing federal estate tax forms may be needed or desired. Federal estate taxes are levied on estates larger than $13.99 million dollars in 2025, meaning that the first $13.99 million dollars of an estate are exempt from federal estate taxes. The following table is used for amounts over the $13.99 million dollar exemption.

2025 Federal Estate Tax Table:

| Tax rate | Taxable amount | Tax owed |

|---|---|---|

the amount over $10,000 | ||

the amount over $20,000 | ||

the amount over $40,000 | ||

the amount over $60,000 | ||

the amount over $80,000 | ||

the amount over $100,000 | ||

the amount over $150,000 | ||

the amount over $250,000 | ||

the amount over $500,000 | ||

the amount over $750,000 | ||

the amount over $1,000,000 |

It is good practice to file the final accounting with the probate court to resolve any claims against the estate. An estate settlement agreement may be used instead of a final accounting. After the personal representative pays all debts and taxes, estate assets will be distributed to beneficiaries stated in the will, or by laws of intestacy if there is no will. They must also prepare the final accounting. The final accounting shows assets contained within the estate, how the personal representative managed assets, and how assets were distributed to beneficiaries.

Next Steps for Settling an Estate in Pennsylvania

Settling an estate in Pennsylvania can be a straightforward process with the right preparation and materials. Understanding what probate is and which assets can be omitted from the probate process can help direct your estate planning and ease the process of settling your estate later. Whether you’re just starting your financial planning journey or putting your affairs in order, a financial advisor can help guide you so that your estate settlement will be clearer.

This article is meant to give a brief overview of the steps involved in settling or administering an estate in PA and does not constitute estate planning advice.

Consult an estate attorney regarding legal advice and a CERTIFIED FINANCIAL PLANNER™ practitioner for financial advice.