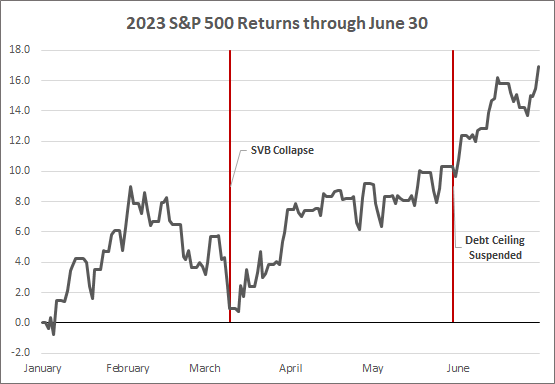

The most telegraphed recession in history must wait a little longer before coming to fruition. Economic data through the first half of the year remained mixed, with the labor market and service industries remaining strong. However, manufacturing is experiencing some weakness paired with still sticky inflation. Despite the mixed messages, stocks did not waiver much, and the S&P 500 Index closed the first half of the year up 16.9%. Although it was a robust six months for the S&P 500, the standout performer was the Nasdaq Composite Index, led by large technology stocks, closing the first half of the year with a 32% gain.

2023 has shown the return of the proverbial Wall of Worry, meaning stocks continue to trade higher despite risks being present. Similar environments were the COVID rally in 2020, the U.S.-China trade war in 2019, and the U.S. Presidential Election and Brexit in 2016 which all presented economic or geopolitical risks dominating headlines. But, equities continued to grind higher during each period, hence climbing the Wall of Worry. In fact, most of this year’s gain came after the Regional Banking Crisis in March, when multiple banks failed over the course of a few weeks- and we cannot forget about the debt ceiling drama before Memorial Day.

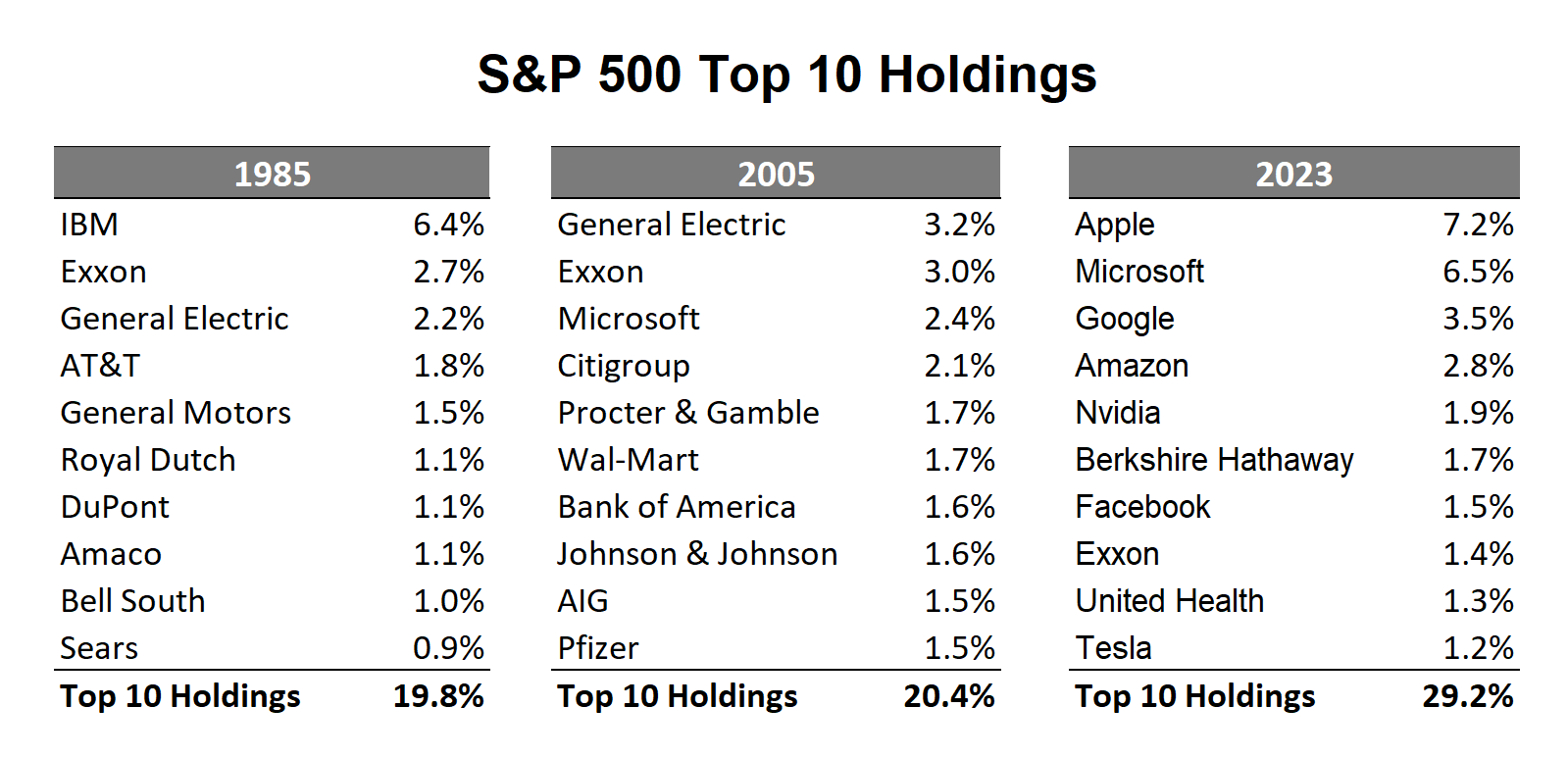

This year, much of the S&P 500 Index’s gain has been driven by excitement around technology and artificial intelligence, but also the prospect of a new bull market for stocks and the index approaching a new all-time high for the first time in over eighteen months. One concern investors have discussed this year is the few stocks that have been driving returns. Removing the ten largest companies from the market capitalization-weighted S&P 500 Index has led to returns being close to flat this year, rather than the over 16% return we see from the whole. This also explains why the Dow Jones Average is only up 5% this year, as the more stable blue chip companies have not participated in the rally.

Like many topics, there are two sides to the index concentration issue. On the positive side, owning top performing companies can be a profitable investment. In June, Apple became the first $3 trillion company, larger than the total market value of the 600 stock United Kingdom market. However, is owning over 7% of Apple, like the index, too big of a bet on a forward-looking basis? In the 1980s, IBM was the largest company in the index, more than double the weight of the second largest company, Exxon. In 2005, Apple was not even in the top ten largest companies and General Electric was the biggest. As index composition changes over multi-year periods, this presents opportunities to invest in the next era of growth. Still, at the same time, there is a risk of being heavily invested in the current largest companies if the next growth era is negative for that group.

At the time of this writing, the top ten stocks in the index make up about 30%, but it’s also important to remember the other 70%. Last quarter the best-performing stocks in the S&P 500 Index were the three cruise lines, not the technology companies that have been dominating headlines. Despite what headlines convey, opportunities exist outside the top companies.